By

Our retirement is not our parents’ retirement. For many American employees in their generation, a good job meant access to a secure retirement income they could not outlive. Employers took center stage, assuming most of the financial risk of funding that retirement with employees largely removed from the process. Today, employers are far more likely to be facilitators of retirement saving, playing a critical supporting role while the employee is the star planner of the retirement show.

How did the idea that employers should offer secure retirement benefits through defined benefit plans, or pensions, evolve? How and why did this change over time to put more of the responsibility on employees to save through defined contribution plans such as 401(k)s? And how can benefits managers use new savings tools and employee benefits available today to help their employees retire smarter, happier and more financially secure?

The U.S. Retirement System

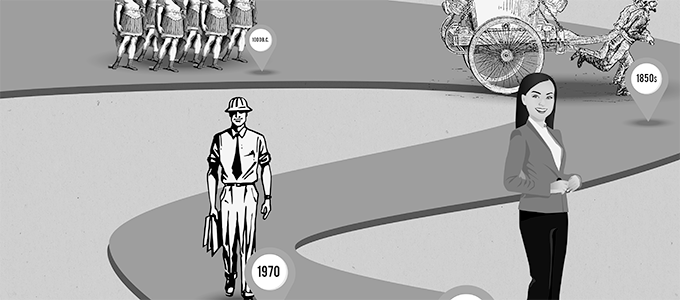

Retirement is a fairly modern concept with origins in military history. Until the late 1800s, those who had to work to earn their living worked their entire lives. Historians credit the Roman Empire with conceiving the idea of an income that continued after work service by

Today, we think of a pension as a …Read More

Read more here:: Work Force Recruitment Feed